Buying a new home is one of the most exciting life-steps a person can take. It’s the opening chapter of a young adult’s coming-of-age story, marks the beginning a new chapter for growing families, or it can mean the realization of a greenside dream in retirement.

This all sounds very romantic, right?

That’s because it is.

BUT.

Before you unlock the door for the first time and the dream becomes a reality, there are many important factors to consider.

One of the most important parts of purchasing a new home is determining the down payment, and considering how this commitment will affect your financial health moving forward.

So, what do you need to know about down payments?

How much do I have to put down?

The answer to this question needs to be approached from a couple of different angles as your required down payment is affected by the home’s purchase price.

At the most basic level, homebuyers must apply a down payment of at least five percent on the first $500,000 of a new home. Once the price of a home increases, 10 percent is required for the purchase price up to $999,999.

For example, if the purchase price of your home is $250,000, the minimum down payment is $12,500.

If the purchase price is $600,000? The minimum required down payment is five percent on the first $500,000, totalling $25,000. On the remaining $100,000, 10 percent is required, totalling $10,000. The combined totals place your minimum down payment at $35,000.

Looking for a home valued over $1,000,000? If so, your required down payment increases to 20 percent of the purchase price.

But wait, there’s more. What about mortgage default insurance?

There’s a little bit more to your down payment than the required percentages above (if life could only be that simple).

As a homebuyer, if your down payment totals less than 20 percent of the home’s purchase price, you must obtain mortgage default insurance, which is offered through the Canada Mortgage and Handling Corporation (CMHC), Genworth and Canada Guaranty.

Mortgage insurance is intended to protect lenders against losses in the event of default payments.

This doesn’t mean you, of course.

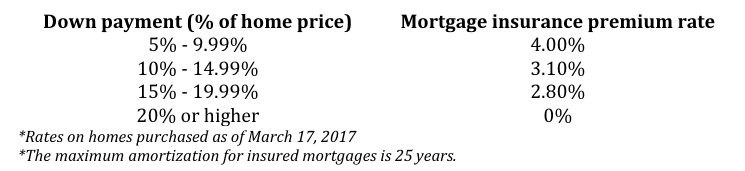

It’s important to understand that mortgage default insurance premiums are tiered depending on the size of your down payment.

So how does this all look? Here’s an example.

You buy a home for $250,000 and secure it with the minimum down payment of five percent. As shown above, the down payment is $12,500.

Take your down payment off of the purchase price ($250,000 – $12,500) and you now have to secure a mortgage on the balance of $237,500.

Now, multiply the amount of your mortgage by the insurance premium. In this case that’s four percent ($237,500 x 4% = $9500).

In this case, your mortgage loan premium is $9,500.

This premium can be paid as a lump sum or incorporated into your mortgage. It’s best to explore what financial scenario works best for you. A mortgage calculator is a great tool for this.

And if you’re like many people and have questions about mortgage insurance, contact an advisor at your local credit union to get the full details.

Yes. Your down payment affects your mortgage.

How much you put down on a home is going to affect your mortgage payments. A bigger down payment can mean thousands of do llars saved in interest over the long-term.

While it’s important to factor in your down payment when it comes to big-picture financial planning, it’s equally important to explore the best options for mortgage rates, as this will play an essential role in determining affordability.

Luckily for homebuyers, there are some good mortgage rates available. For example, Northern Credit Union is currently offering a 5-Year Fixed Rate Mortgage with rates as low as 3.25% and the option of flexible payments. Plus you can apply online which makes things super easy.

In the end.

At any stage in life, buying a home is one of the most significant financial steps most people will ever take. And the down payment is essential to making your dreams come true. Being informed on how the rules factor in to your plans makes the process more comfortable, and allows you to make the best decisions that fit your needs and goals.